Gods of the World

Thursday, July 19, 2012

Wednesday, July 04, 2012

Shadow banking... Emerging Markets.....

Just a thought on the flow of funds from zerohedge....

The growth in Emerging Market 'External Liquidity' recently was only ever slower in the quarters either side of the crash in 2008. This is a very worrying sign. EM nations are highly dependent on 'external' capital inflows (to smooth current account deficits) and have empirically been exposed to the 'sudden stop' nature of these inflows. It appears that Europe's banking crisis and deleveraging is indeed having a critical impact on EM nations - which may oddly mean domestic policy adjustments will be necessary (raising rates to encourage capital inflows) that will further exacerbate the problems as global growth slows. As we note that the more deposit-free the banking system, the slower the funds will flow. The newer the debt- and asset-inflation-based 'capitalism', the faster it is impacted at the margin - and it appears many EM nations are being affected rather rapidly. Here is a chart :

The growth in Emerging Market 'External Liquidity' recently was only ever slower in the quarters either side of the crash in 2008. This is a very worrying sign. EM nations are highly dependent on 'external' capital inflows (to smooth current account deficits) and have empirically been exposed to the 'sudden stop' nature of these inflows. It appears that Europe's banking crisis and deleveraging is indeed having a critical impact on EM nations - which may oddly mean domestic policy adjustments will be necessary (raising rates to encourage capital inflows) that will further exacerbate the problems as global growth slows. As we note that the more deposit-free the banking system, the slower the funds will flow. The newer the debt- and asset-inflation-based 'capitalism', the faster it is impacted at the margin - and it appears many EM nations are being affected rather rapidly. Here is a chart :

Thursday, June 28, 2012

Tuesday, May 08, 2012

Tuesday, April 10, 2012

Banker, Tailor, Soldier, Spy

PRESIDENT OBAMA recently nominated Jim Yong Kim, the president of Dartmouth, to be the next president of the World Bank — a privilege accorded to the United States since the bank’s founding in 1946. A European, in turn, gets to run the International Monetary Fund.

In the wake of World War II, such a divvying up of the top spots among the great powers was inevitable. But how did the United States, the primary founder and financer of the two institutions, wind up taking the helm of the World Bank, and not the I.M.F., which was of vastly greater importance to its government?

In fact, that was the original goal of Harry Dexter White, the Treasury Department’s key representative at the Bretton Woods conference of July 1944, where the two institutions were created. The I.M.F. was central to White’s vision of a postwar global financial architecture dominated by the American dollar.

White relegated the British delegation head, John Maynard Keynes, to the commission creating the World Bank specifically to keep him away from the main event: creating the I.M.F. White so masterfully outmaneuvered the British that they wound up signing on to a dollar-centric design for the fund, one they thought they had already blocked.

Then, on Jan. 23, 1946, Harry S. Truman nominated White to be the first American executive director of the I.M.F. (such directors representing the major member countries). Truman was also widely expected to nominate White for the fund’s top post of managing director.

But trouble soon arose in the form of J. Edgar Hoover, the F.B.I. director. White had been under surveillance for two months, suspected of being a Soviet spy. Hoover prepared a report for the president, based on information provided by 30 sources, including the confessed spy Elizabeth Bentley, asserting that White was “a valuable adjunct to an underground Soviet espionage organization,” who was placing individuals of high regard to Soviet intelligence inside the government. If word of his activities became public, Hoover stressed, it could jeopardize the survival of the fund.

Oblivious, the Senate Committee on Banking and Currency approved White’s nomination on Feb. 5, the day after Hoover’s report was delivered. Secretary of State James F. Byrnes, having read the report, wanted Truman to withdraw the nomination; Treasury Secretary Fred M. Vinson wanted White out of government entirely. Truman, who did not trust Hoover but who knew he had a major political problem on his hands, decided to quarantine White as the American I.M.F. executive director, a huge step down from managing director.

Nominating another American to sit above White, however, would have raised red flags. Why was the fund’s chief architect being passed over? It was a question the White House wished to avoid.

On March 5, Vinson met with Keynes, now the British governor of both the I.M.F. and the World Bank. He said Truman had decided not to put White’s name forward for the I.M.F. top job, despite his being “ideally suited” for it. The United States would, instead, back an American for the World Bank. Keynes was shocked.

Washington got its way, of course, and a Belgian, Camille Gutt, became the first head of the I.M.F., while an American, Eugene Meyer, became the first head of the World Bank. Though the United States was clearly in a powerful enough position to claim the I.M.F. job after Gutt’s departure in 1951, the fund was for the moment effectively moribund, its role supplanted by the Marshall Plan, and the United States was content keeping the World Bank post.

As for White, he resigned from the I.M.F. in 1947. The next summer Bentley and Whittaker Chambers accused him of spying for the Soviets, a charge he denied before the House Un-American Activities Committee on Aug. 13. He died of a heart attack three days later.

Following Alger Hiss’s perjury conviction in 1950, Representative Richard M. Nixon revealed a handwritten memo of White’s given to him by Chambers, apparently showing that White had passed classified information for transmission to the Soviets. Yet his guilt would only be firmly established after publication of Soviet intelligence cables in the late 1990s. Instead of treating the World Bank presidency as a sacred American birthright, we should remember that it was never more than a consolation prize for an administration trying to dodge a spy scandal.

By BENN STEIL

Monday, April 09, 2012

JPMorgan Trader’s Positions Said to Distort Credit Indexes

Straight from Bloomberg: The London Whale

A JPMorgan Chase & Co. (JPM) trader of derivatives linked to the financial health of corporations has amassed positions so large that he’s driving price moves in the $10 trillion market, traders outside the firm said.

The trader is London-based Bruno Iksil, according to five counterparts at hedge funds and rival banks who requested anonymity because they’re not authorized to discuss the transactions. He specializes in credit-derivative indexes, a market that during the past decade has overtaken corporate bonds to become the biggest forum for investors betting on the likelihood of company defaults.

Though Iksil reveals little to other traders about his own positions, they say they’ve taken the opposite side of transactions and that his orders are the biggest they’ve encountered. Two hedge-fund traders said they have seen unusually large price swings when they were told by dealers that Iksil was in the market. At least some traders refer to Iksil as “the London whale,” according to one person in the business.

Joe Evangelisti, a spokesman for New York-based JPMorgan, declined to comment on Iksil’s specific transactions. Iksil didn’t respond to phone messages and e-mails seeking comment.

The Markit CDX North America Investment Grade Index of credit-default swaps Series 18 (IBOXUMAE) rose 3.3 basis points to 100.2 basis points as of 10:18 a.m. in New York, after jumping 4.4 basis points yesterday, according to Markit Group Ltd. The price of the index is quoted in yield spreads, which rise along with the perceived likelihood of increased corporate defaults.

A credit-default swap is a financial instrument that investors use to hedge against losses on corporate debt or to speculate on a company’s creditworthiness.

Iksil may have “broken” some credit indexes -- Wall Street lingo for creating a disparity between the price of the index and the average price of credit-default swaps on the individual companies, the people said. The persistence of the price differential has frustrated some hedge funds that had bet the gap would close, the people said.

Iksil, unlike JPMorgan traders who buy and sell securities on behalf of customers, works in the chief investment office. The unit is affiliated with the bank’s treasury, helping to control market risks and investing excess funds, according to the lender’s annual report.

“The chief investment office is responsible for managing and hedging the firm’s foreign-exchange, interest-rate and other structural risks,” Evangelisti said. It’s “focused on managing the long-term structural assets and liabilities of the firm and is not focused on short-term profits.”

Iksil probably traded under close supervision at JPMorgan, said Paul Miller, an analyst at FBR Capital Markets in Arlington, Virginia.

“The issue is how much capital they’re putting at risk,” said Miller, a former examiner for the Federal Reserve Bank of Philadelphia.

Wall Street banks including JPMorgan, Goldman Sachs Group Inc. and Morgan Stanley have submitted comment letters and met with regulators to discuss their complaints about the rule.

“Several agencies claiming jurisdiction over the Volcker rule have proposed regulations of mind-numbing complexity,” JPMorgan Chief Executive Officer Jamie Dimon said in his annual letter to shareholders released this week. “Even senior regulators now recognize that the current proposed rules are unworkable and will be impossible to implement.”

Chief Investment Officer Ina Drew, who runs the unit, was among JPMorgan’s highest-paid executives in 2011, earning $14 million, a 6.8 percent pay cut from 2010, the bank said in a regulatory filing this week. Drew referred a request for comment to Evangelisti.

Iksil has earned about $100 million a year for the chief investment office in recent years, the Wall Street Journal said in an article following Bloomberg News’s initial report, citing people familiar with the matter.

Iksil joined JPMorgan in 2005, according to his career- history record with the U.K. Financial Services Authority. He worked at the French investment bank Natixis (KN) from 1999 to 2003, according to data compiled by Bloomberg.

The trader may have built a $100 billion position in contracts on Series 9 (IBOXUG09) of the Markit CDX North America Investment Grade Index, according to the people, who said they based their estimates on the trades and price movements they witnessed as well as their understanding of the size and structure of the markets.

The positions, by the bank’s calculations, amount to tens of billions of dollars and were built with the knowledge of Iksil’s superiors, a person familiar with the firm’s view said.

A JPMorgan Chase & Co. (JPM) trader of derivatives linked to the financial health of corporations has amassed positions so large that he’s driving price moves in the $10 trillion market, traders outside the firm said.

The trader is London-based Bruno Iksil, according to five counterparts at hedge funds and rival banks who requested anonymity because they’re not authorized to discuss the transactions. He specializes in credit-derivative indexes, a market that during the past decade has overtaken corporate bonds to become the biggest forum for investors betting on the likelihood of company defaults.

Investors complain that Iksil’s trades may be distorting prices, affecting bondholders who use the instruments to hedge hundreds of billions of dollars of fixed-income holdings. Analysts and economists also use the indexes to help gauge perceptions of risk in credit markets.

Though Iksil reveals little to other traders about his own positions, they say they’ve taken the opposite side of transactions and that his orders are the biggest they’ve encountered. Two hedge-fund traders said they have seen unusually large price swings when they were told by dealers that Iksil was in the market. At least some traders refer to Iksil as “the London whale,” according to one person in the business.

Joe Evangelisti, a spokesman for New York-based JPMorgan, declined to comment on Iksil’s specific transactions. Iksil didn’t respond to phone messages and e-mails seeking comment.

Most-Active Index

The credit indexes are linked to the default risk on a group of at least 100 companies. The newest and most-active index of investment-grade credit rose the most in almost four months yesterday and climbed again today.The Markit CDX North America Investment Grade Index of credit-default swaps Series 18 (IBOXUMAE) rose 3.3 basis points to 100.2 basis points as of 10:18 a.m. in New York, after jumping 4.4 basis points yesterday, according to Markit Group Ltd. The price of the index is quoted in yield spreads, which rise along with the perceived likelihood of increased corporate defaults.

A credit-default swap is a financial instrument that investors use to hedge against losses on corporate debt or to speculate on a company’s creditworthiness.

Iksil may have “broken” some credit indexes -- Wall Street lingo for creating a disparity between the price of the index and the average price of credit-default swaps on the individual companies, the people said. The persistence of the price differential has frustrated some hedge funds that had bet the gap would close, the people said.

Close Supervision

Some traders have added positions in a bet that Iksil eventually will liquidate some holdings, moving prices in their favor, the people said.Iksil, unlike JPMorgan traders who buy and sell securities on behalf of customers, works in the chief investment office. The unit is affiliated with the bank’s treasury, helping to control market risks and investing excess funds, according to the lender’s annual report.

“The chief investment office is responsible for managing and hedging the firm’s foreign-exchange, interest-rate and other structural risks,” Evangelisti said. It’s “focused on managing the long-term structural assets and liabilities of the firm and is not focused on short-term profits.”

Iksil probably traded under close supervision at JPMorgan, said Paul Miller, an analyst at FBR Capital Markets in Arlington, Virginia.

“The issue is how much capital they’re putting at risk,” said Miller, a former examiner for the Federal Reserve Bank of Philadelphia.

Volcker Rule

A U.S. curb on proprietary trading at banks, meant to reduce the odds they’ll make risky investments with their own capital, is supposed to take effect in July. Regulators are still determining how the so-called Volcker rule will make exceptions for instances where firms are hedging to curtail risk in their lending and trading businesses.Wall Street banks including JPMorgan, Goldman Sachs Group Inc. and Morgan Stanley have submitted comment letters and met with regulators to discuss their complaints about the rule.

“Several agencies claiming jurisdiction over the Volcker rule have proposed regulations of mind-numbing complexity,” JPMorgan Chief Executive Officer Jamie Dimon said in his annual letter to shareholders released this week. “Even senior regulators now recognize that the current proposed rules are unworkable and will be impossible to implement.”

Combined Revenue

JPMorgan had $4.14 billion of combined revenue last year from the chief investment office, treasury and private-equity investments, according to the annual report. The treasury and chief investment office held a combined $355.6 billion of investment securities as of December 2011, up 14 percent from a year earlier, according to a year-end earnings statement.Chief Investment Officer Ina Drew, who runs the unit, was among JPMorgan’s highest-paid executives in 2011, earning $14 million, a 6.8 percent pay cut from 2010, the bank said in a regulatory filing this week. Drew referred a request for comment to Evangelisti.

Iksil has earned about $100 million a year for the chief investment office in recent years, the Wall Street Journal said in an article following Bloomberg News’s initial report, citing people familiar with the matter.

Iksil joined JPMorgan in 2005, according to his career- history record with the U.K. Financial Services Authority. He worked at the French investment bank Natixis (KN) from 1999 to 2003, according to data compiled by Bloomberg.

Trader’s Position

The French-born trader commutes to London each week from Paris and works from home most Fridays, the Journal article said, citing a person who worked with him.The trader may have built a $100 billion position in contracts on Series 9 (IBOXUG09) of the Markit CDX North America Investment Grade Index, according to the people, who said they based their estimates on the trades and price movements they witnessed as well as their understanding of the size and structure of the markets.

The positions, by the bank’s calculations, amount to tens of billions of dollars and were built with the knowledge of Iksil’s superiors, a person familiar with the firm’s view said.

Sunday, March 04, 2012

Here is my newest paper: Market Commentary for Q1 2012

Here is the link to download the full paper:

http://www.mediafire.com/?m145mdavdhmsrhj

Topics in this edition includes:

1. The battle for the reserve currency status

2. How to save Greece and why the Euro is a failed experiment

3. History of the gold standard and the IMF

4. Q2 US yield curve trade strategy

5. Canadian housing market and covered bonds

6. Republican primaries

7. The Syrian and Russian relationship

Enjoy!

http://www.mediafire.com/?m145mdavdhmsrhj

Topics in this edition includes:

1. The battle for the reserve currency status

2. How to save Greece and why the Euro is a failed experiment

3. History of the gold standard and the IMF

4. Q2 US yield curve trade strategy

5. Canadian housing market and covered bonds

6. Republican primaries

7. The Syrian and Russian relationship

Enjoy!

Thursday, March 01, 2012

Greek 1 Year Bond 80% Away From 1000%

As I mentioned in the few articles below or in my market commentary for those of you that read my Q1 2012 paper, Greek paper hit 1000% yield outside period of hyperinflation and here is an article from zerohedge today that follows up:

Today for the first time ever Greek 10 year bonds slide to below 20% of par (5.9% of 2022 dropped to 19.145 cents) as expected some time ago, as increasingly the revulsion to post reorg bonds gets greater and greater courtesy of that now meaningless cash coupon of 2% through 2015. When considering that the country will redefault within a year, it explains why nobody has any interest in holding Greek paper even assuming there is an EFSF bill sweetener. Also, today's ISDA decision did not help. What is most amusing is that as of this morning, the country's 1 Year bonds hit an all time high yield of 920.2%. Well, if Greek bonds crossing 100% just 5 months ago was not quite attractive, perhaps 1000% will. At this rate we expect said threshold to cross some time today.

Today for the first time ever Greek 10 year bonds slide to below 20% of par (5.9% of 2022 dropped to 19.145 cents) as expected some time ago, as increasingly the revulsion to post reorg bonds gets greater and greater courtesy of that now meaningless cash coupon of 2% through 2015. When considering that the country will redefault within a year, it explains why nobody has any interest in holding Greek paper even assuming there is an EFSF bill sweetener. Also, today's ISDA decision did not help. What is most amusing is that as of this morning, the country's 1 Year bonds hit an all time high yield of 920.2%. Well, if Greek bonds crossing 100% just 5 months ago was not quite attractive, perhaps 1000% will. At this rate we expect said threshold to cross some time today.

Tuesday, February 21, 2012

As Dow Passes 13,000 In Nominal Terms, Here Is The "Real" Picture

From Zerohedge: Three charts that perhaps will calm the nominal euphoria as Dow 13000 screams across the screens. Since May 2008, the Dow is unchanged in price and down 50% in 'real' gold terms. The picture is just as disheartening from the start of 2011 and 2012. Next stop Dow 20,000 and Gold 20,000?

From May 2008, The Dow priced in Gold is down 50% while we have nominally recovered unchanged.

From the start of 2011. The Dow is up 11.35% while in real terms it is down 12.4%...

and from the beginning of this year, the Dow is up 4.8% while in gold 'real' terms, it is down 4.25%...

Charts: Bloomberg

From May 2008, The Dow priced in Gold is down 50% while we have nominally recovered unchanged.

From the start of 2011. The Dow is up 11.35% while in real terms it is down 12.4%...

and from the beginning of this year, the Dow is up 4.8% while in gold 'real' terms, it is down 4.25%...

Charts: Bloomberg

Wednesday, February 01, 2012

Thursday, January 26, 2012

¥1,086,000,000,000,000 (Quadrillion) In Debt And Rising

And since I spent much of my time studying the lost decades, here is a pretty interesting article posted at Zerohedge in regards to US and Japanese monetary policies:

Yesterday the Japanese Finance Ministry made a whopper of an announcement: in the year ending March 2013, total Japanese debt will surpass one quadrillion yen, or ¥1,086,000,000,000,000. This is roughly in line with the Zero Hedge expectations that by this March total Japanese debt would surpass one quadrillion yen. In USD terms, at today's exchange rate, this is precisely $14 trillion. And while smaller than America's $15.4 trillion (net of all post debt ceiling breach auctions), which was $14 trillion about a year ago, the GDP backing this notional amount of debt, which just so happens is greater than the GDP of the entire Euro area, is a modest ¥481 trillion, so by the end of the next fiscal year, Japan will have a Debt to GDP ratio of 225%. And that's not counting all the household and financial debt. So prepare to add quadrillion to the vernacular. At this exponential rate of increase quintillion will appear some time in 2015 and so on. Yet the scariest conclusion is that as Bloomberg economist Joseph Brusuelas points out, America is not only next, it already is Japan. Actually scratch that, America is worse than Japan, which at least generated a real housing bubble in the years just preceding the onset of its multi-decade credit crunch, something not even America could do in comparable terms. More importantly, "the debt-to-GDP ratio of the U.S. recently surpassed 100 percent, and it did so in the four years after the onset of the recession, compared with the six years it took the Japanese debt-to-GDP ratio to do so." The Japanese may be better than America in most things, but when it comes to destroying its economy, the US has no equal. Brusuelas' conclusion: "If below trend growth is the most probable scenario in the U.S., the most likely alternative is that the U.S. economy is headed for a lost decade… or two." So... go all in?

From Bloomberg's Brusuelas:

Yesterday the Japanese Finance Ministry made a whopper of an announcement: in the year ending March 2013, total Japanese debt will surpass one quadrillion yen, or ¥1,086,000,000,000,000. This is roughly in line with the Zero Hedge expectations that by this March total Japanese debt would surpass one quadrillion yen. In USD terms, at today's exchange rate, this is precisely $14 trillion. And while smaller than America's $15.4 trillion (net of all post debt ceiling breach auctions), which was $14 trillion about a year ago, the GDP backing this notional amount of debt, which just so happens is greater than the GDP of the entire Euro area, is a modest ¥481 trillion, so by the end of the next fiscal year, Japan will have a Debt to GDP ratio of 225%. And that's not counting all the household and financial debt. So prepare to add quadrillion to the vernacular. At this exponential rate of increase quintillion will appear some time in 2015 and so on. Yet the scariest conclusion is that as Bloomberg economist Joseph Brusuelas points out, America is not only next, it already is Japan. Actually scratch that, America is worse than Japan, which at least generated a real housing bubble in the years just preceding the onset of its multi-decade credit crunch, something not even America could do in comparable terms. More importantly, "the debt-to-GDP ratio of the U.S. recently surpassed 100 percent, and it did so in the four years after the onset of the recession, compared with the six years it took the Japanese debt-to-GDP ratio to do so." The Japanese may be better than America in most things, but when it comes to destroying its economy, the US has no equal. Brusuelas' conclusion: "If below trend growth is the most probable scenario in the U.S., the most likely alternative is that the U.S. economy is headed for a lost decade… or two." So... go all in?

From Bloomberg's Brusuelas:

The Long Malaise: Similarities Between Japan And The US

Slowly and surely, comparisons between the long malaise in Japan and the historically weak expansion in the U.S. are growing more valid.

These similarities primarily relate to the unique problems following the piercing of a debt-financed asset bubble that left many households, banks and firms with liabilities that exceeded assets following the bursting of a residential asset bubble. Unless policy is put in place soon or unless home prices are allowed to adjust to equilibrium clear-ing levels, it is growing more likely that the U.S. economy will continue to underperform in a fashion eerily similar to that of Japan over the past two decades. While differences between the U.S. and Japanese economies are many – the conspicuous consumption practiced by American consumers versus the thriftier Japanese public, for example – the similarities between the two economies are many. The direction of long-term yields and of the housing sector, as well as the increasingly leveraged U.S. balance sheet, look all too similar to Japan following the piercing of that country’s housing and equity market bubbles.

Peak to trough, home prices are down 33 percent. The Japanese housing market did not experience appreciable pricing gains during the first two decades of recovery, not exactly a comforting thought for either home owners or policy makers. A comparison between Japan and the U.S. housing markets in the four years following the bursting of their respective housing bubbles shows the two markets headed down the same listless path.

From the viewpoint of policy makers, the floundering housing market is blocking the process through which accommodative financial conditions stoke economic growth. This is likely why the Fed is considering purchasing mortgage-backed securities. It is also why PresidentObama, in his State of the Union address, expressed the desire to create a refinancing program that would support even the refinancing of mortgages not owned or guaranteed by Fannie Mae and Freddie Mac.

Meanwhile, the debt-to-GDP ratio of the U.S. recently surpassed 100 percent, and it did so in the four years after the onset of the recession, compared with the six years it took the Japanese debt-to-GDP ratio to do so. This makes it difficult for policy makers to push forward fiscal solutions to the housing problem, especially given private investor concern over the sovereign debt crisis in the euro zone.

Since the onset of the recession in the U.S., the economy has grown above the long-term trend of 2.7 percent in only three of 16 quarters, averaging a scant 0.16 percent rate of growth. This is very similar to the 0.5 percent average level of growth in Japan between 1991-2000. If below trend growth is the most probable scenario in the U.S., the most likely alternative is that the U.S. economy is headed for a lost decade… or two. Until a solution is put forward that addresses the shadow inventory of homes and permits prices to adjust, policy makers are just spinning their wheels, engaging in stop-gap measures that will probably prove insufficient to solve the most vexing of problems.

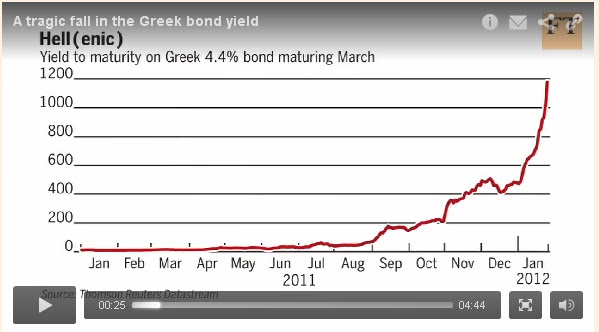

Another interesting Greece chart

Since I still don't understand why they are so stupid and continue to negotiate till today with Merkel instead of just leaving the Euro and establishing their own monetary policy, here is something interesting that i came across FT today...

Take a look at this chart, Greece is officially the first country to have bonds to yield over 1000% outside periods of hyperinflation...

Take a look at this chart, Greece is officially the first country to have bonds to yield over 1000% outside periods of hyperinflation...

But at least the short end of the yield curve for Spain is looking better today than 2 months ago so...

Subscribe to:

Posts (Atom)